Container ship orderbook hits 6.5m TEU for the first time since 2008

The container ship orderbook hit a post-financial crisis low just below 2m TEU in October 2020. In the eighteen months since then, liner operators have seen record profits and a large percentage of these have been poured into newbuilding contracts.

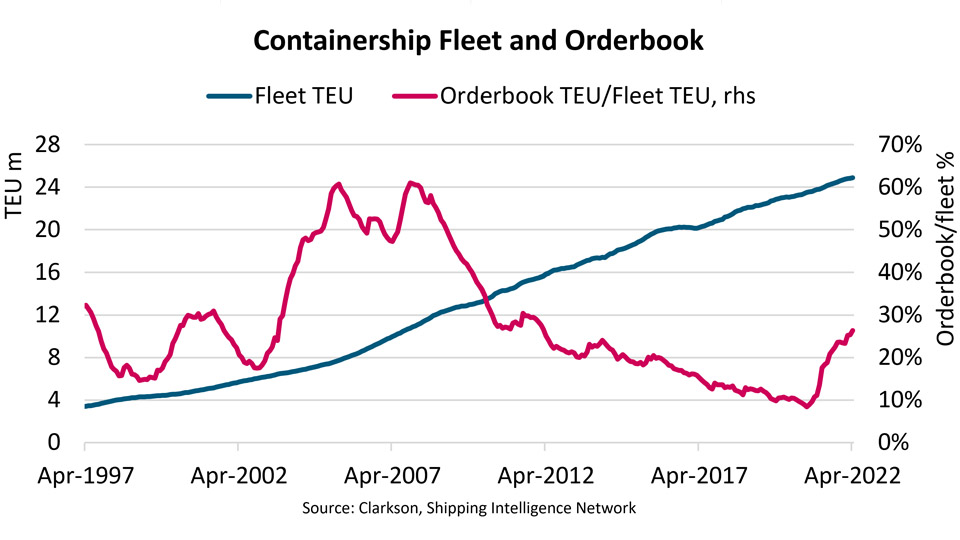

In just eighteen months, 6m TEU of newbuilding contracts have been added to the container ship orderbook. This has taken the orderbook past 6.5m TEU for the first time since late 2008.

The orderbook is now 26% of the fleet size for the first time since 2014 and, combined with YTD 2022 deliveries, 6.2m TEU are now scheduled to be delivered during 2022-2024.

In addition to the newbuilding deliveries, we must expect that congestion problems around the world will eventually begin to ease. This could release as much as 2m TEU effective supply on top of newbuilding deliveries, and the total additional supply appears to be on target to exceed 8m TEU between early 2022 and early 2025, representing 33% of the current fleet size in just three years.

In the meantime, on the other side of the supply equation, demolition and sailing speed are very likely also headed for substantial changes. A share of the fleet will not be able to comply with EEXI targets without retrofits or introduction of Engine Power Limitation (EPL). Some vessels may, however, have no good path to compliance while remaining commercially attractive and will be demolished.

The vessels that do achieve EEXI compliance will also be faced with CII introduction on 1 January 2023 as well as shipping’s likely inclusion in the EU’s Emission Trading Scheme (ETS). This will add further pressure on reducing GHG emissions and some vessels may simply be considered uneconomical to keep in operation. Others may have to slow down further to achieve the desired CII rating.

Most owners probably already have plans in place for their individual vessels. However, accurately estimating the impact of EEXI, CII, and ETS on the entire fleet is extremely difficult.

All that seems certain is that we will see more vessels demolished and others reducing speed. Because of the reduced speed, liner operators may have to add an additional vessel to several services. Still, unless demand surprises on the upside it appears unlikely that all the capacity being delivered and released from congestion can be absorbed without damaging the supply/demand balance in the coming years.

Feedback or a question about this information?

Posted:

07 April 2022

BIMCO's Shipping number of the week

- Iron ore shipments up 3.8% despite weak Chinese demand

- COVID pandemic wiped 24.6 million TEU off container market growth

- EU tanker import tonne mile demand up 12% as ships avoid Red Sea area

- Demand shocks drive ship recycling to lowest level in 20 years

- 13% of world seaborne trade under attack from Houthis and Somali pirates

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.