US dirty tanker export demand jumps 33% year-on-year

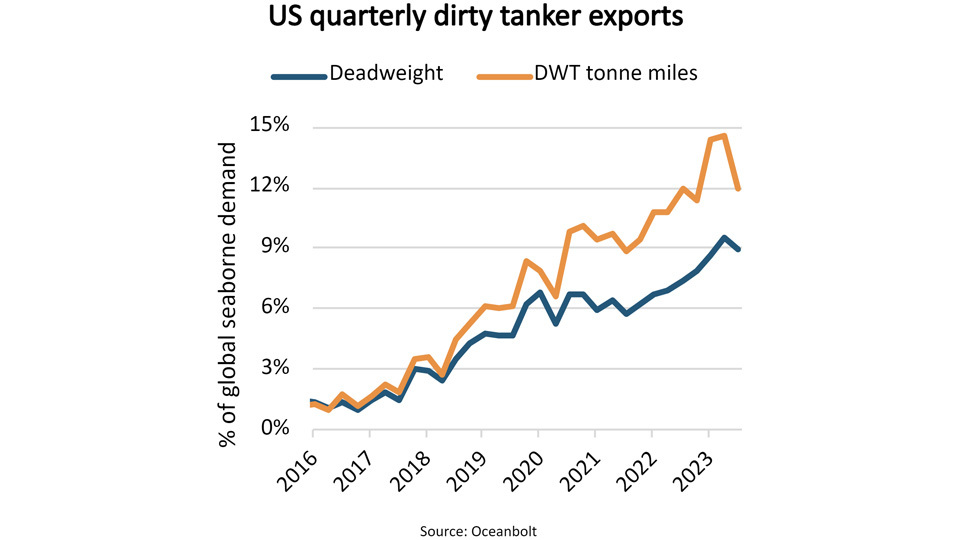

During the first eight months of 2023, US dirty tanker export demand increased 33% year-on-year while the global dirty tanker exports increased only 5%. Measured in deadweight tonne miles, US exports now account for 14% of global dirty tanker demand.

US oil production has increased since 2013 while US refinery runs peaked before the COVID pandemic. This has allowed dirty tanker exports to increase from 0.4 million barrels per day (mbpd) in 2016 to 3.5 mbpd during the first eight months of 2023. During the same period export deadweight tonne miles have grown at an average annual pace of 46% and increased from 1% to 14% of global dirty tanker demand.

Exports into East Asia have grown particularly fast in recent years, making the region the largest destination area since 2019, now accounting for 20% of the dirty tanker ship capacity departing the US.

The shift in exports towards East Asia has further added to ship demand growth by increasing average sailing distances by one third since 2016.

The increased trade with East Asia has resulted in a rise in shipments on Very Large Crude Carriers (VLCCs). Year-to-date 2023 they have accounted for 69% of all US export deadweight tonne miles, a 10 percentage points increase compared to 2022.

Due to the EU’s sanction on Russian oil exports, US dirty tanker exports have grown the fastest into the EU since 2021. In 2023, average monthly deadweight tonne miles from the US to the EU have more than doubled compared with 2021. This has further added to the growth in demand for VLCCs which in 2023 account for 43% of deadweight tonne miles into the EU, up from just 2% in 2021.

All in all, the increase in US oil production and the shifts in trade patterns have made the US the second largest contributor to dirty tanker export demand, only exceeded by Saudi Arabia. In the future the US will contribute even more.

The International Energy Agency (IEA) estimates that that the US will contribute one third of the increase in global oil production between 2023 and 2028. However, US refinery runs are expected to decline during that period. US seaborne exports and their share of global dirty tanker demand are therefore expected to increase further.

Feedback or a question about this information?

Posted:

13 September 2023

BIMCO's Shipping number of the week

- Iron ore shipments up 3.8% despite weak Chinese demand

- COVID pandemic wiped 24.6 million TEU off container market growth

- EU tanker import tonne mile demand up 12% as ships avoid Red Sea area

- Demand shocks drive ship recycling to lowest level in 20 years

- 13% of world seaborne trade under attack from Houthis and Somali pirates

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.