RECORDED WEBINAR: Tanker Shipping Market Overview & Outlook Q1 2023: The stars align to create the strongest market in 15 years

Overview

Although risks remain, all indicators point to solid and sustained market strength not seen since the financial crisis hit in 2008.

Highlights

- Demand will grow faster than supply during both 2023 and 2024.

- In 2024, we predict that crude tanker demand will be up 4.5-6.5% on 2022, whereas supply will reduce by 0.6%. Similarly, we envisage product tanker demand growth of 6-8%, with supply falling 0.7%.

- Freight rates, time charter rates, and second-hand ship values will all see gains throughout 2023 and 2024.

- Renewed growth in China and increased demand for jet fuel following the reopening of travel to and from China are key drivers of cargo demand growth.

- In addition, we expect that an increase of 3-4% in average sailing distances following the EU’s ban on Russian oil and oil products will add to tonne miles demand.

- Fleet growth is limited by very small order books. Combined with predicted reduction in sailing speeds of 2-3% due to decarbonisation regulations, overall supply will fall.

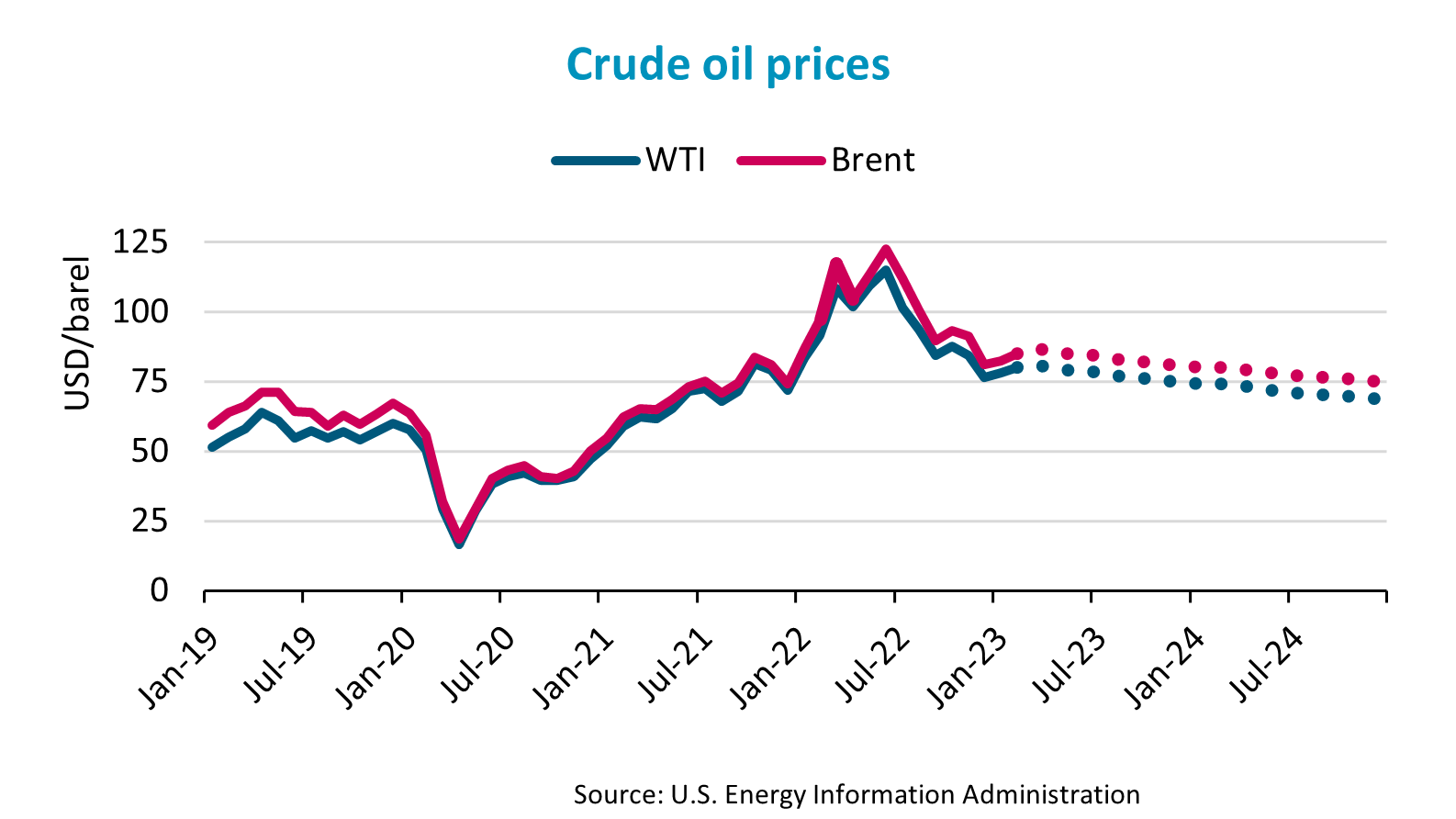

- The EIA predicts that oil prices will fall throughout 2023 and 2024 and that Brent will dip below USD 80/barrel in 2024.

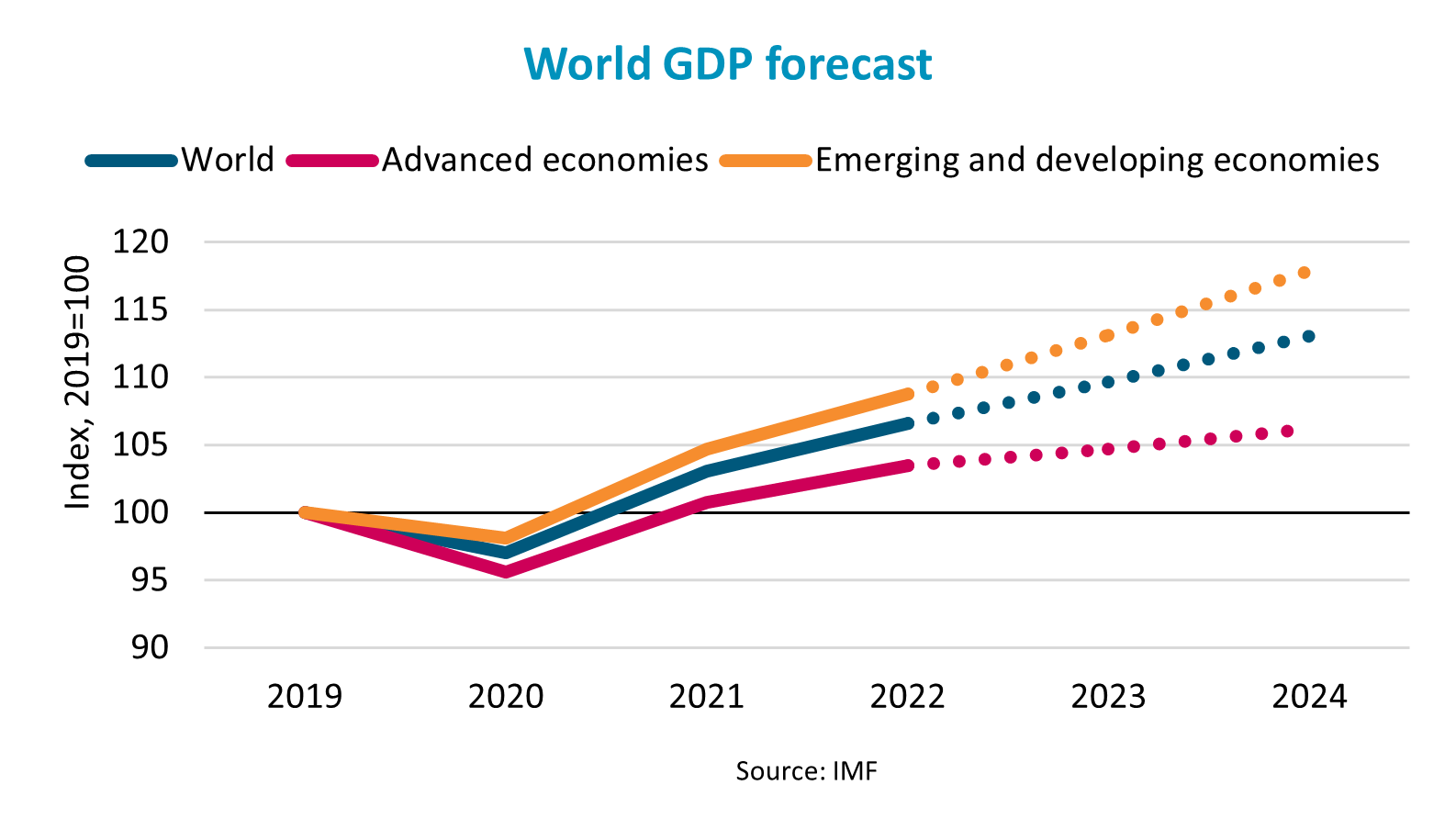

- The IMF predicts global GDP growth of 2.9% in 2023 and 3.1% in 2024 but highlights that the balance of risks remains weighted on the downside.

- Risks to our forecast therefore remain. Cargo demand would suffer from lower economic growth and predicted structural shifts have yet to be seen.

Demand drivers

Although both the crude and product tanker markets have faced challenges during the past few months, we maintain our upbeat outlook for 2023 and 2024. In 2023, we estimate cargo demand to grow by 0-1% for crude tankers and by 1.5-2.5% for product tankers, whereas we expect growth of 1-2% for both sectors in 2024. Compared to our previous report, this means slightly slower growth in 2023 but faster in 2024. However, we still predict a 3-4% increase in average sailing distances for both sectors this year due to the change in trading patterns following the EU’s ban on Russian oil imports.

The US Energy Information Administration (EIA) predicts an increase in liquid fuels consumption of 1.1 mbpd (1.1%) in 2023 and 1.8 mbpd (1.8%) in 2024, ending next year at a record high of 102.3 mbpd. The International Energy Agency (IEA) predicts faster growth, and that consumption will hit 101.9 mbpd in 2023.

Increased growth in China and the end of the country’s COVID-19 and travel restrictions are expected to be key drivers of growth. Increased jet fuel demand is predicted to account for at least half of new demand.

The IMF has revised its growth forecast for the global economy to 2.9% (+ 0.2 pp) in 2023 and 3.1% (- 0.1 pp) in 2024. The key driver of the improvement in 2023 is an improved outlook for the Chinese economy following the relaxation of COVID-19 restrictions. This has led the IMF to increase estimated growth in China to 5.2% in 2023 (up from 4.4%), while the estimate for 2024 has been maintained at 4.5%.

Economic growth in advanced economies has been revised to 1.2% (+ 0.1 pp) in 2023 and 1.4% (- 0.2 pp) in 2024. For both years, predictions for USA and the major Euro Area economies have been increased slightly, while those for other major advanced economies have been lowered, although only the UK economy is forecast to contract and end 2024 smaller than it was in 2022.

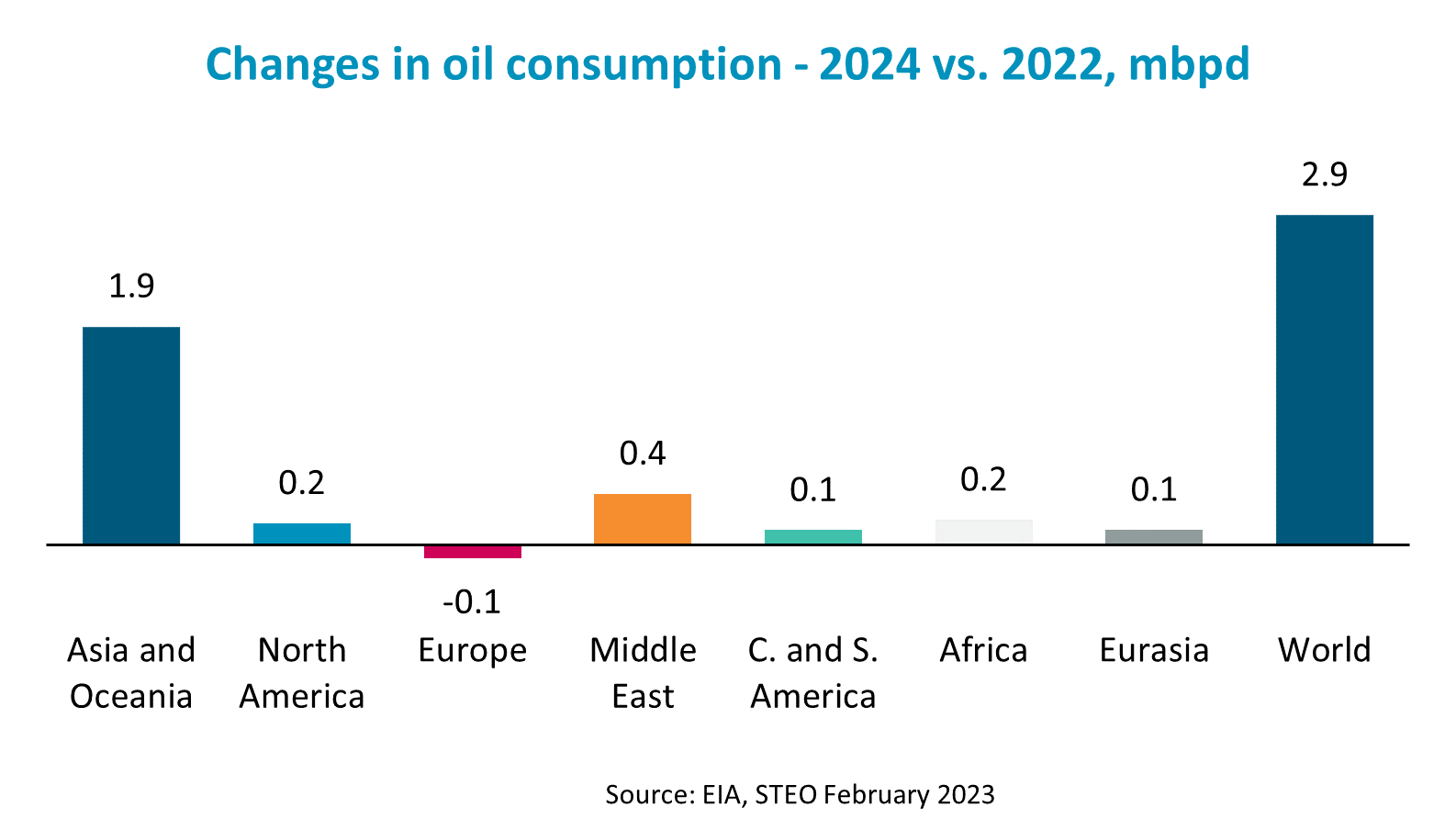

The EIA predicts that China will account for 38% of the growth in oil demand between 2022 and 2024, with India accounting for 18%. The Middle East will account for another 15% of growth. The remainder is split across other regions. Notably, however, demand in Europe is expected to decline further and end 4% lower than in 2022 and 6% lower than in 2019.

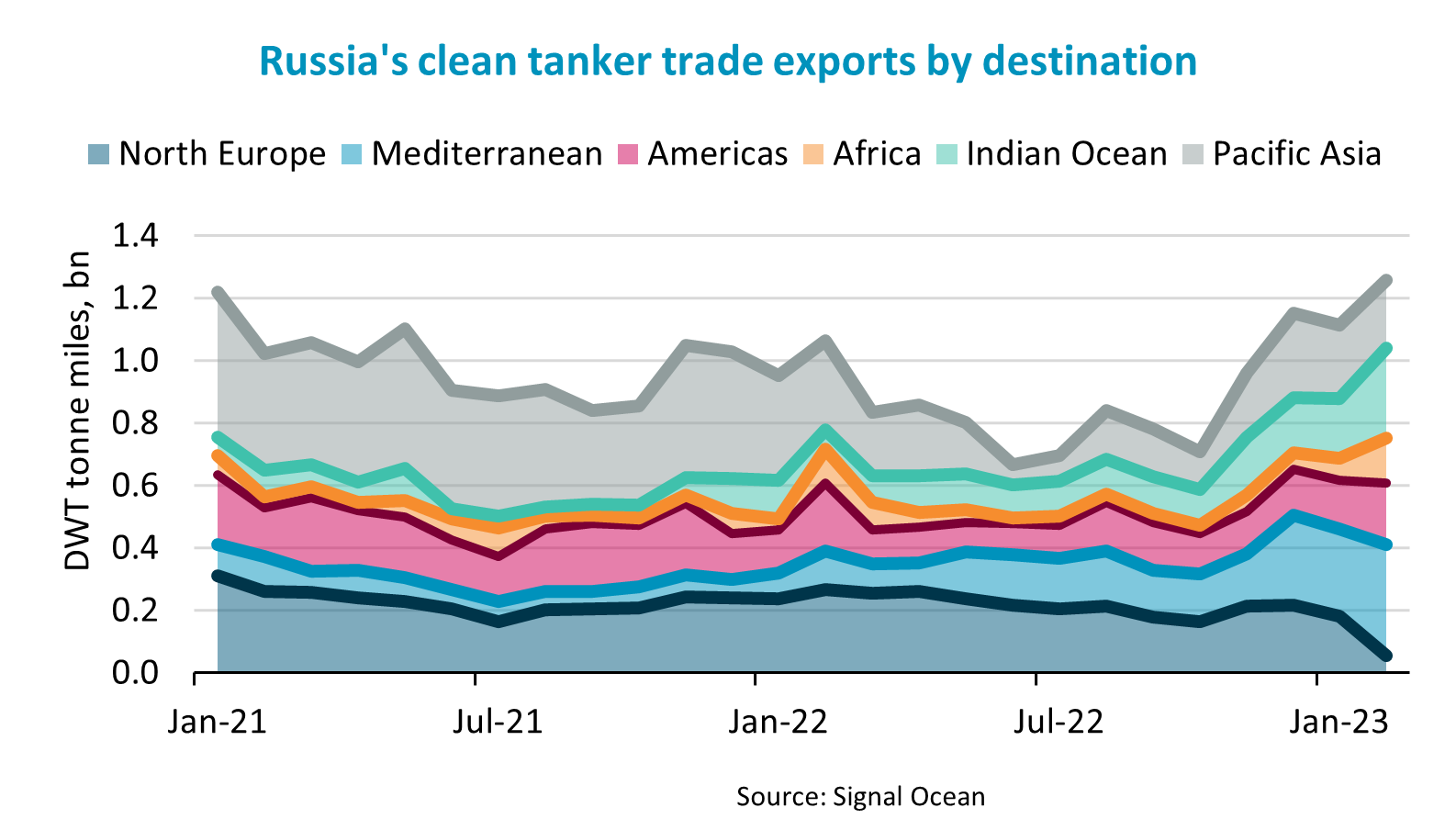

Global production is forecast to be 2.0 mbpd higher in 2024 than in 2022. Production in North America will increase by 1.8 mbpd, with the US supplying 73% of this. Russian production will reduce by 1.1 mbpd. This is a smaller reduction than previously predicted as it appears that Russia has become more successful in finding new buyers for its oil.

Russian crude exports have been shifted to India, China, and destinations in the Mediterranean. Russian export dirty tanker trade tonne miles are so far on average 24% higher in February 2023 than in November 2022 (before the EU ban), and more than double than a year ago. The transition of the clean tanker trade has also begun, and new buyers have been found in the Mediterranean, Asia, and the Americas. So far, average tonne miles are up 13% m/m in February 2023 and 23% y/y.

Oil prices have fallen quite significantly from the highs of 2022 and the EIA predicts that prices will continue to slide. The average brent price is expected to end at USD 84/barrel in 2023 and USD 78/barrel in 2024, down from an average of USD 101/barrel in 2022. This should support an increase in demand.

Supply drivers

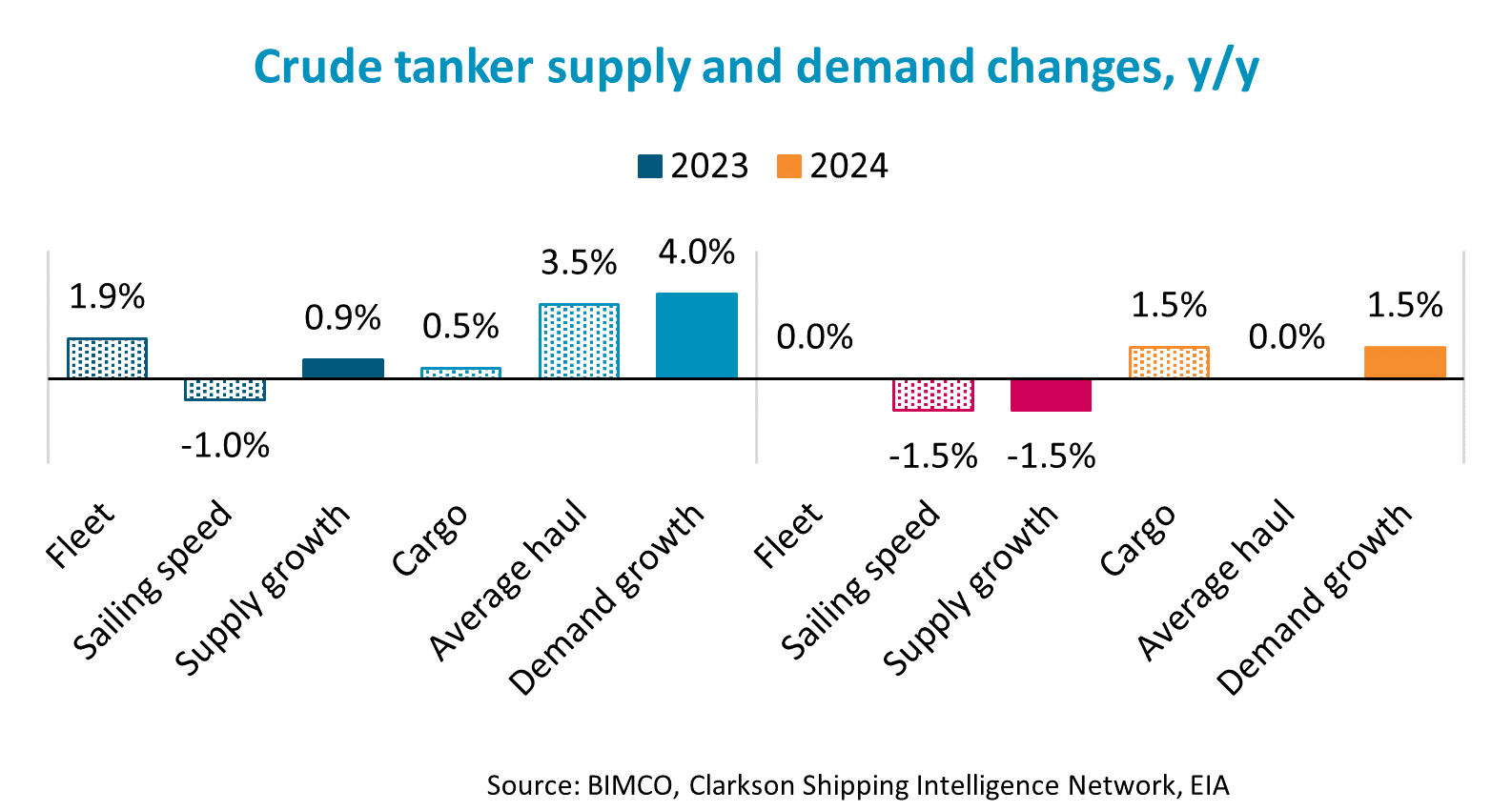

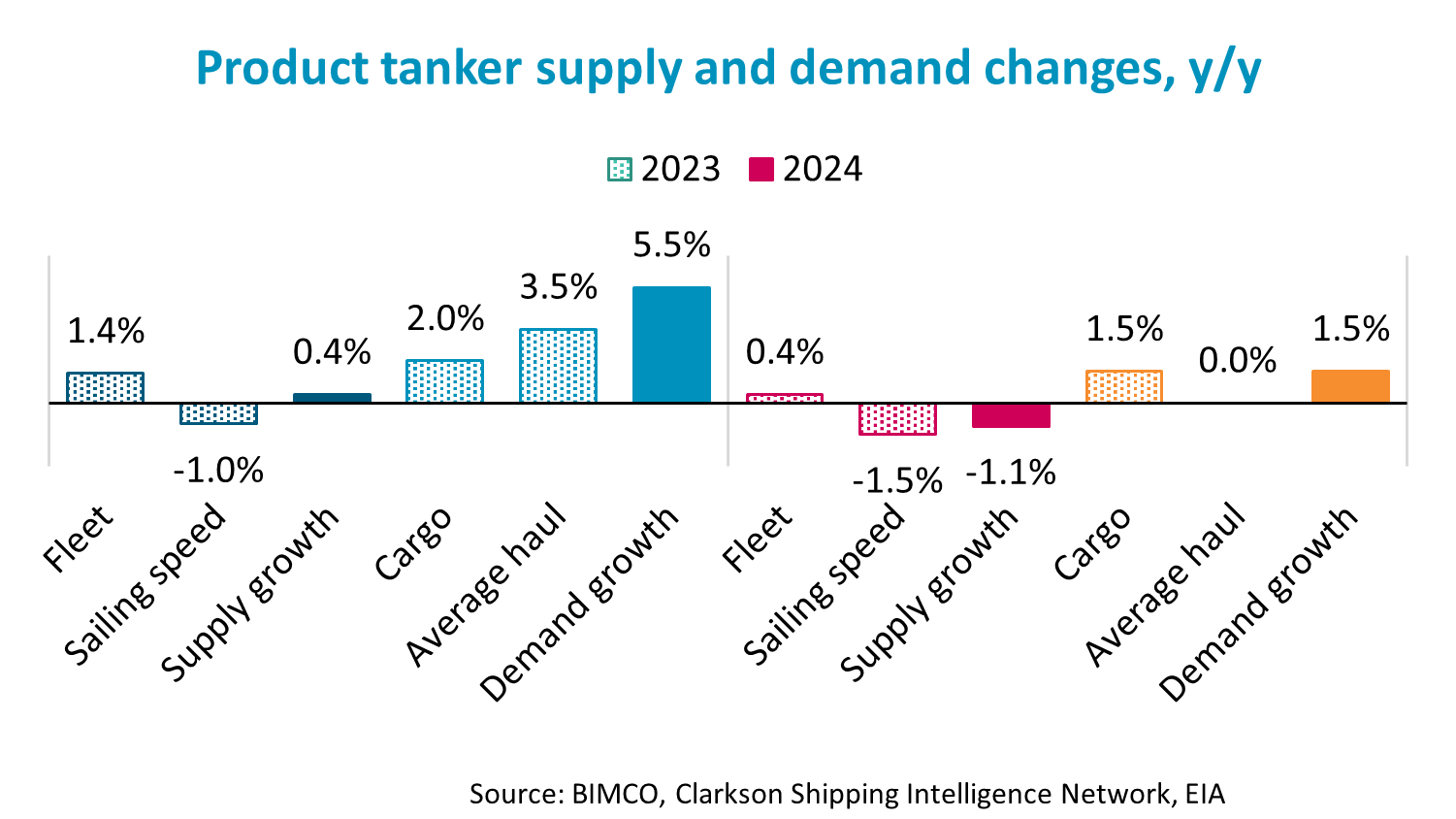

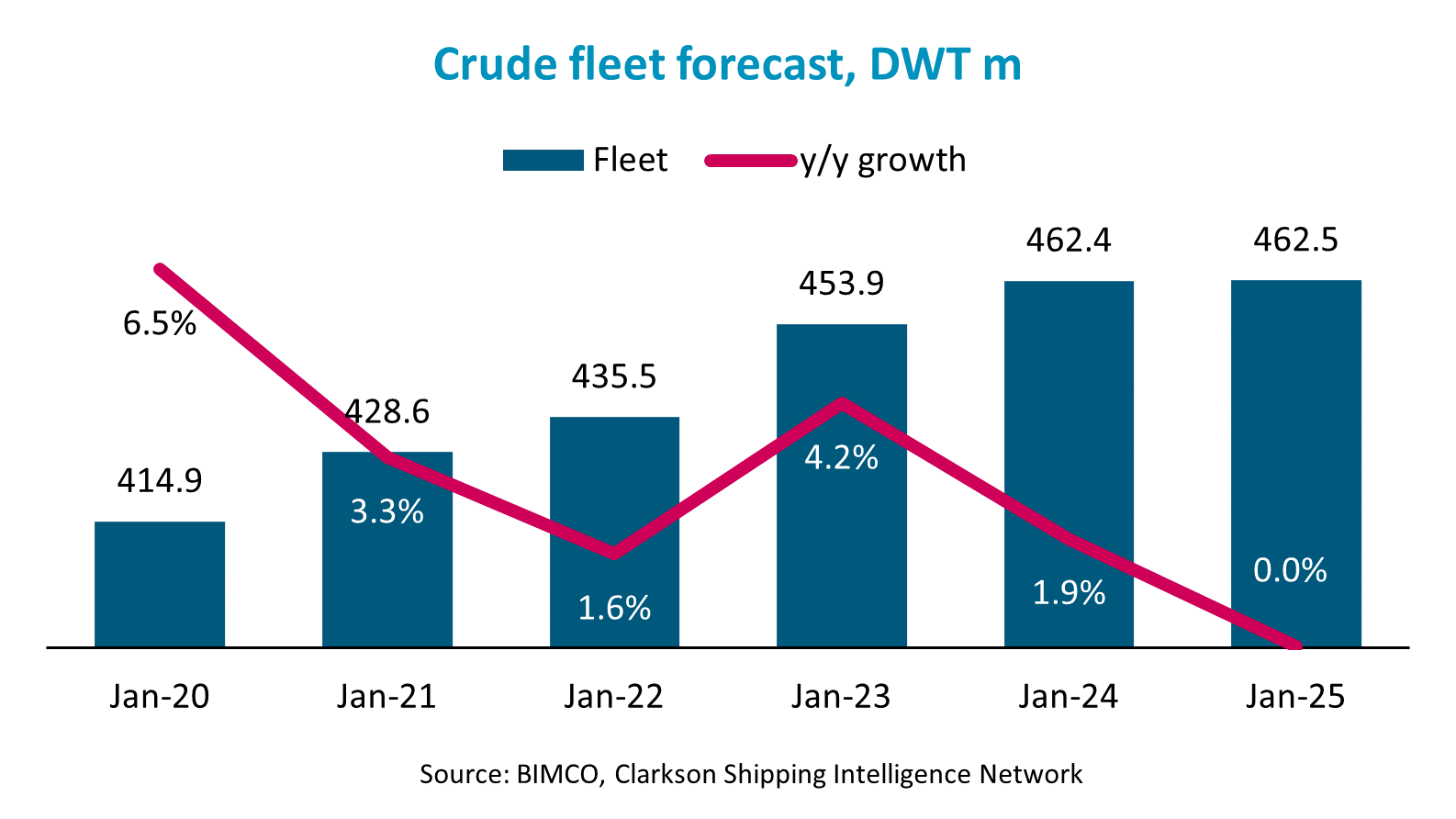

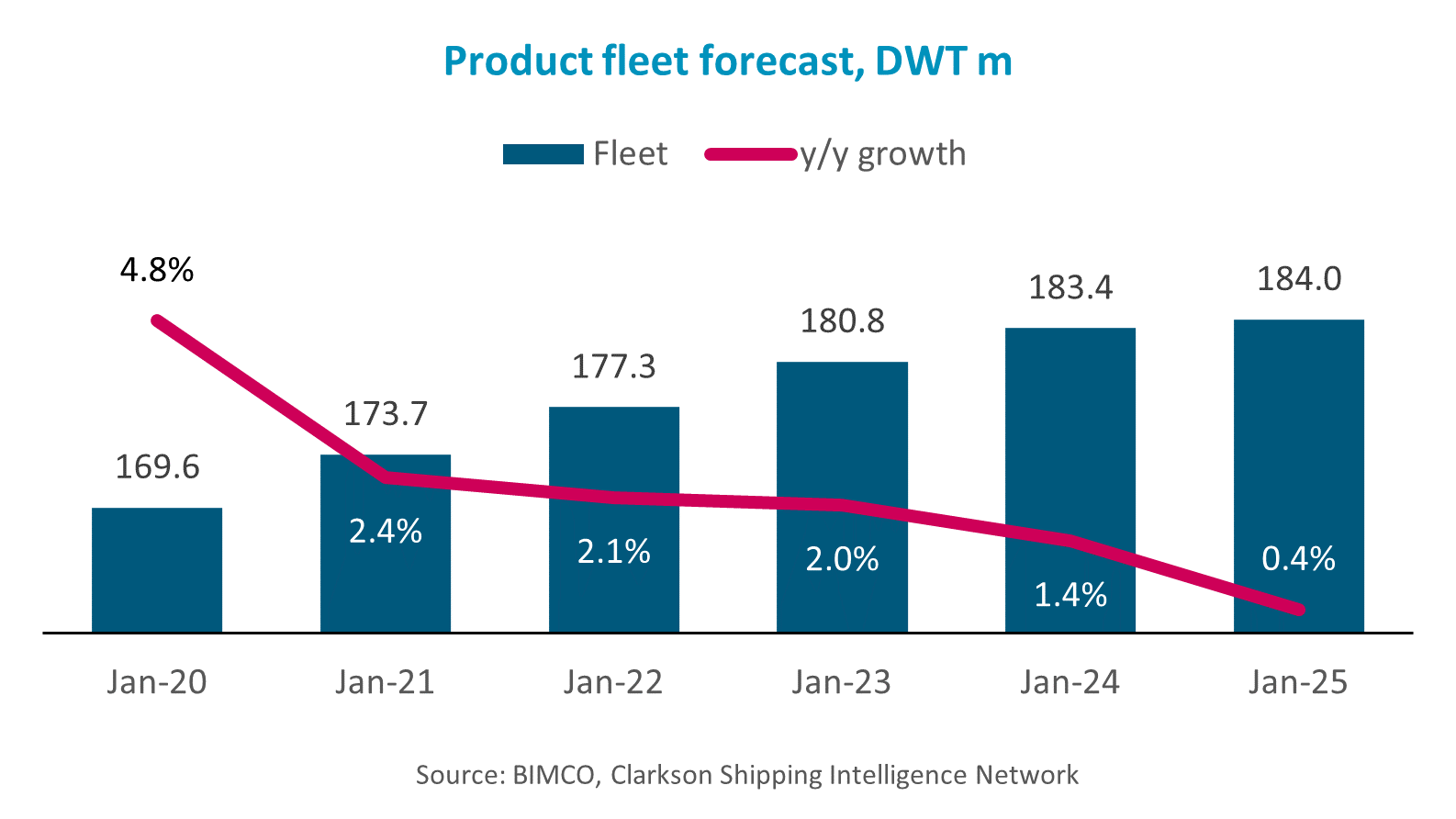

We estimate fleet growth of 1.9% for crude tankers and 1.4% for product tankers in 2023, with respective figures of 0.0% and 0.4% for each fleet in 2024.

Very small order books of 5.4% and 4.4% vs. fleet size for crude and product tankers respectively, combined with estimated recycling, will keep fleet growth in check.

In addition, we expect that fleet productivity will reduce as sailing speed is reduced in order to comply with EEXI and CII regulations. However, compared to our previous report, we now estimate that the impact of this will be partly seen only in 2024; consequently, we estimate speed reductions of 0.5-1.5% in 2023 and 1-2% in 2024.

Contracting is likely to pick up as the order book depletes and owners enjoy sustained profits. Slight decreases in newbuilding prices may even be a possibility if contracting of container and LNG ships slows down and forward cover is reduced at shipyards. This could present an opportunity for owners to contract new ships that are designed to comply with future decarbonisation regulations.

All in all, actual crude tanker supply is estimated to grow by 0.9% in 2023 and decline by 1.5% in 2024. Product tanker supply should grow by 0.4% in 2023 and fall by 1.1% in 2024.

Conclusion

Our forecast predicts that crude tanker demand will grow faster than supply by 2.5-3.5 pp in both 2023 and 2024. The product tanker market will fare even better, with demand outpacing supply by 4.5-5.5 pp in 2023 and by 2-3 pp in 2024.

Unsurprisingly, we predict that the tightening of the supply/demand balance will lead to an increase in freight rates, time charter rates, and second-hand ship prices.

We believe in fact that the market will experience a period of sustained market strength that has not been seen since the 2008 financial crisis.

Obviously, risks to our forecast remain. Cargo demand is heavily dependent on renewed growth in China leading to increased domestic demand as well as growth in global jet fuel demand as travel to and from China reopens. Cargo supply could be hurt should Russia fail to sustain oil product exports and China again curtails export quotas.

Although the supply/demand balance could still tighten even if average hauls do not increase or sailing speeds do not decrease, both factors are key drivers of the significant strength that we predict. Should either of these shifts in trade and operational patterns not materialise as predicted, the market will not strengthen as per our forecast.

Even without these structural shifts, the supply/demand balance will, however, still be stronger in 2024 than in 2022 if our fleet and cargo growth estimates are accurate. As such, it will take quite a few unpredicted changes to fully undermine the predicted improved strength of the markets.

REGISTER FOR THE WEBINARS ON 1 AND 2 MARCH

READ THE CONTAINER REPORT AND THE DRY BULK REPORT

Feedback or a question about this information?

Posted:

28 February 2023

Updated: 02 March 2023

VPS Bunker Alerts

Veritas Petroleum Services (VPS) publish regular Bunker Alerts based entirely on fuel samples and have kindly permitted BIMCO’s Members to access this information.

The Bunker Alerts are not intended to be an evaluation of overall bunker quality in the port or area concerned, but usually highlight a specific parameter within the fuel which has raised a quality issue.

Latest ice reports for members

Latest piracy reports

Latest industry releasable threats

Related publication

Road to recovery

In 2016 the dry bulk shipping sector experienced some of the worst market conditions in history. In response, BIMCO produced a unique analysis model, named "Roa...

In 2016 the dry bulk shipping sector experienced some of the worst market conditions in history. In response, BIMCO produced a unique analysis model, named "Roa...

ELSEWHERE ON BIMCO

Contracts & Clauses

All of BIMCO's most widely used contracts and clauses as well as advice on managing charters and business partners.

Learn about your cargo

For general guidance and information on cargo-related queries.

BIMCO Publications

Want to buy or download a BIMCO publication? Use the link to get access to the ballast water management guide, the ship master’s security manual and many other publications.

About a new business partner

We can help members check new business partners. We also help to recover millions of USD (undisputed) funds every year.